Have you heard? Refresh Financial has been officially acquired by Borrowell, Canada’s leading credit education company and one of the country’s largest fintech companies. The Toronto-based company has helped over 1.5 million Canadians access their credit score and report, while also providing personalized credit coaching tools and financial product recommendations based on their credit profile. With Borrowell’s mission to make financial stability possible for all Canadians and our mission to help Canadians from any background build a better financial reputation, the two companies make the perfect match! Here’s what Refresh founder and CEO, Michael Wendland, has to say about the exciting news. “Borrowell has been a great partner for many years and I am truly excited about further integrating Refresh’s products into their platform. I know that as a combined organization, we can play an important role during these times in providing Canadians from all backgrounds with access to credit, helping them not only manage today but thrive tomorrow.” As Borrowell’s co-founder and CEO, Andrew Graham states, being part of the Borrowell team will allow Refresh to offer a wider range of financial tools and products to clients. “With an expanded team across the country and a comprehensive suite of credit building solutions, we’re eager to help even more Canadians access credit products that meet their specific needs and maximize their long-term financial health. All Canadians deserve a fair shot at building credit history, accessing affordable credit, and reaching their financial goals. We believe we can help make that a reality.” By combining forces with Borrowell, Refresh Financial can reach even more underserved Canadians and provide them with tangible credit building solutions. Together, we can help all Canadians build a better financial reputation and achieve their goals. If you’re a Refresh Financial customer, this acquisition doesn’t impact your account or your current standing with us. You can still reach out to your client representative with any questions or concerns you may have about your account with us. Check out Borrowell’s full press release!

Have you heard? Refresh Financial has been officially acquired by Borrowell, Canada’s leading credit education company and one of the country’s largest fintech companies. The Toronto-based company has helped over 1.5 million Canadians access their credit score and report, while also providing personalized credit coaching tools and financial product recommendations based on their credit profile. With Borrowell’s mission to make financial stability possible for all Canadians and our mission to help Canadians from any background build a better financial reputation, the two companies make the perfect match! Here’s what Refresh founder and CEO, Michael Wendland, has to say about the exciting news. “Borrowell has been a great partner for many years and I am truly excited about further integrating Refresh’s products into their platform. I know that as a combined organization, we can play an important role during these times in providing Canadians from all backgrounds with access to credit, helping them not only manage today but thrive tomorrow.” As Borrowell’s co-founder and CEO, Andrew Graham states, being part of the Borrowell team will allow Refresh to offer a wider range of financial tools and products to clients. “With an expanded team across the country and a comprehensive suite of credit building solutions, we’re eager to help even more Canadians access credit products that meet their specific needs and maximize their long-term financial health. All Canadians deserve a fair shot at building credit history, accessing affordable credit, and reaching their financial goals. We believe we can help make that a reality.” By combining forces with Borrowell, Refresh Financial can reach even more underserved Canadians and provide them with tangible credit building solutions. Together, we can help all Canadians build a better financial reputation and achieve their goals. If you’re a Refresh Financial customer, this acquisition doesn’t impact your account or your current standing with us. You can still reach out to your client representative with any questions or concerns you may have about your account with us. Check out Borrowell’s full press release!  Simple Rate has put together a list of the best Secured Cards available in Canada and Refresh Financial is proud to have been rated as the best overall secured card in Canada for no credit check with guaranteed approval. Simple Rate understands that most people’s financial situations are not the same, and therefore there is no one-size-fits-all credit card. With all the different credit cards on the market today, it can be difficult to find the best one for you. Simple Rate’s mission is to educate Canadians on how to use credit cards effectively to earn the most rewards and cash back. The Value of a Credit Card Credit cards have two main benefits. First, they provide access to funds when you don’t necessarily have the money at the time. That’s why it’s called credit. While you will pay high interest rates when carrying a balance on a credit card, it is nice to have the option to “buy now, pay later”, especially in case of an emergency. Secondly, credit cards are extremely useful in this digital age for making online purchases and reservations. Without a credit card you will find it challenging to rent a car, book a hotel, buy a vacation and more. Credit Cards for Bad Credit When applying for a regular credit card, the lender will check your credit score. It makes sense as they are giving you access to credit. They want assurances that you will pay it back on time, and your credit score reflects that. Upon seeing a poor credit score they are less likely to approve you for a credit card. For Canadians with poor credit, there is less choice of credit cards available to them, and a secured card is sometimes the only – and best – option for spending flexibility while safely building credit. You put down a deposit which in most cases becomes your credit limit. This protects the lender in case you don’t make your monthly payments while giving you the benefits of having a credit card. Used responsibly, a secured credit card allows you to establish a history of repayment of debts which, overtime, boosts your credit score. Learn more about Refresh Financial’s Secured Card and apply online in less than 20 minutes! Guaranteed approval, no credit checks!

Simple Rate has put together a list of the best Secured Cards available in Canada and Refresh Financial is proud to have been rated as the best overall secured card in Canada for no credit check with guaranteed approval. Simple Rate understands that most people’s financial situations are not the same, and therefore there is no one-size-fits-all credit card. With all the different credit cards on the market today, it can be difficult to find the best one for you. Simple Rate’s mission is to educate Canadians on how to use credit cards effectively to earn the most rewards and cash back. The Value of a Credit Card Credit cards have two main benefits. First, they provide access to funds when you don’t necessarily have the money at the time. That’s why it’s called credit. While you will pay high interest rates when carrying a balance on a credit card, it is nice to have the option to “buy now, pay later”, especially in case of an emergency. Secondly, credit cards are extremely useful in this digital age for making online purchases and reservations. Without a credit card you will find it challenging to rent a car, book a hotel, buy a vacation and more. Credit Cards for Bad Credit When applying for a regular credit card, the lender will check your credit score. It makes sense as they are giving you access to credit. They want assurances that you will pay it back on time, and your credit score reflects that. Upon seeing a poor credit score they are less likely to approve you for a credit card. For Canadians with poor credit, there is less choice of credit cards available to them, and a secured card is sometimes the only – and best – option for spending flexibility while safely building credit. You put down a deposit which in most cases becomes your credit limit. This protects the lender in case you don’t make your monthly payments while giving you the benefits of having a credit card. Used responsibly, a secured credit card allows you to establish a history of repayment of debts which, overtime, boosts your credit score. Learn more about Refresh Financial’s Secured Card and apply online in less than 20 minutes! Guaranteed approval, no credit checks!

- the addition of a tool that informs secured card customers when their balance exceeds 30% of their available limit (which can negatively impact your credit score)

- the launch of knowledge base – answers to every possible question we could think of related to Refresh Financial’s products.

Lately, we have had feedback that the wait times to reach our call centre are too long. In most cases, our care agents are answering calls from clients asking questions that are answered directly within your dashboard! If you have a question about the Credit Builder Loan, the Secured Card, reporting to credit bureaus or anything else related to our products and services, navigate to the Knowledge Base from within the Help Centre of your Refresh Dashboard before you call or email us. We’ve built a pretty neat Answerbot to scan through our database of questions and answers so you can quickly and easily find what you’re looking for. Start typing your question in the space available and as you type, all the questions related to what you are asking will be presented to you, with answers. If you aren’t able to get an answer to your question (but we are pretty confident that we have almost every question covered!) you can open a help ticket from within the dashboard to ask your specific question. This is the quickest way to get an answer rather than calling in! Check out Knowledge Base and Answerbot now!

Lately, we have had feedback that the wait times to reach our call centre are too long. In most cases, our care agents are answering calls from clients asking questions that are answered directly within your dashboard! If you have a question about the Credit Builder Loan, the Secured Card, reporting to credit bureaus or anything else related to our products and services, navigate to the Knowledge Base from within the Help Centre of your Refresh Dashboard before you call or email us. We’ve built a pretty neat Answerbot to scan through our database of questions and answers so you can quickly and easily find what you’re looking for. Start typing your question in the space available and as you type, all the questions related to what you are asking will be presented to you, with answers. If you aren’t able to get an answer to your question (but we are pretty confident that we have almost every question covered!) you can open a help ticket from within the dashboard to ask your specific question. This is the quickest way to get an answer rather than calling in! Check out Knowledge Base and Answerbot now!  Have you heard of bad credit loans? Your credit score is one of the biggest factors – sometimes the only factor – that goes into determining if you will be approved for a loan. In most cases, if your credit score is too low you will be denied a loan as the lender views you as too high of a risk to lend to. There are, however, some lenders that are prepared to loan money to anyone, even people with a low credit score. Bad credit loans may seem like a good idea, but in reality, they should be avoided unless you’re absolutely desperate. Never take out one of these loans for a ‘want’ such as a new car, a bigger TV, or a vacation. They should be taken out with extreme caution for something unavoidable. Here’s why: The Drawbacks of Bad Credit Loans in Canada A bad credit loan is risky for the lender for two reasons: (i) bad credit loans are unsecured. If you do not make your repayment, the lender has no way of recouping their money. (ii) borrowers with lower credit score are more likely to not-repay the loan – their low credit score has indicated that this has happened in the past.

Have you heard of bad credit loans? Your credit score is one of the biggest factors – sometimes the only factor – that goes into determining if you will be approved for a loan. In most cases, if your credit score is too low you will be denied a loan as the lender views you as too high of a risk to lend to. There are, however, some lenders that are prepared to loan money to anyone, even people with a low credit score. Bad credit loans may seem like a good idea, but in reality, they should be avoided unless you’re absolutely desperate. Never take out one of these loans for a ‘want’ such as a new car, a bigger TV, or a vacation. They should be taken out with extreme caution for something unavoidable. Here’s why: The Drawbacks of Bad Credit Loans in Canada A bad credit loan is risky for the lender for two reasons: (i) bad credit loans are unsecured. If you do not make your repayment, the lender has no way of recouping their money. (ii) borrowers with lower credit score are more likely to not-repay the loan – their low credit score has indicated that this has happened in the past.- To compensate for these risks, lenders charge a premium interest rate. Whereas with a good credit score you might pay 5% in interest for a cash loan, with a bad credit loan you may be paying up to 50%! The reason for this is that the lender is trying to recoup as much of their money early on as possible, before the likelihood of defaulting on the loan gets higher.

- Bad credit loan providers have sometimes been known to be predatory lenders, charging many hidden fees to ensure they get as much money out of a desperate borrower as possible, although the regulatory landscape for bad credit loans has tightened in recent years.

- You may find yourself in an endless cycle of debt with bad credit loans. Borrowers often find themselves unable to afford to make the full payments and subsequently, roll their debt over into a new loan, which includes more fees and high interest. It can be a situation that becomes impossible to get out of.

This is a question we have often been asked here at Refresh. There is a belief that if you are not using a credit card, the account should be closed to increase your credit score. But is that correct? The short answer is no. In fact, closing a credit card account that you are no longer using could do the opposite and have a negative impact on your credit score. It all comes down to how you are using your other sources of credit.

This is a question we have often been asked here at Refresh. There is a belief that if you are not using a credit card, the account should be closed to increase your credit score. But is that correct? The short answer is no. In fact, closing a credit card account that you are no longer using could do the opposite and have a negative impact on your credit score. It all comes down to how you are using your other sources of credit.Let’s take a deeper look.

In this scenario, Bob has three credit cards and a line of credit. His line of credit is $10,000 and he’s used $4,000 of it on home renovations. His credit card limits are $2,500, $10,000 and $5,000. On each of those cards, his balance is $1,000, $3,000 and $0.- Line of credit: $4,000 used of $10,000

- Credit card 1: $1,000 used of $2,500

- Credit card 2: $3,000 used of $10,000

- Credit card 3: $0 used of $5,000

- Total available credit = $27,500

- Total balances = $8,000

- Credit usage percentage = 29% – a credit usage percentage under 30% is going to help increase your credit score. Over 30% and it will start have an increasingly negative affect on your credit score.

- Line of credit: $4,000 used of $10,000

- Credit card 1: $1,000 used of $2,500

- Credit card 2: $3,000 used of $10,000

- Credit card 3: $0 used of $5,000

- Total available credit = $22,500

- Total balances = $8,000

- Credit usage percentage = 35% – Bob’s credit usage percentage has increase from 29% to 35% without him doing anything. Over 30% and this figure is going to start having a negative affect on his score.

What should Bob do?

The right course of action for Bob depends on his personal circumstance and his spending habits. Bob is a big spender, and he is easily tempted by the available credit and knows that if he doesn’t close his credit card account he might end up spending it. So, he must weigh up the options:- Option A: Keep the account open and keep his credit score moving in the right direction – but risk spending the credit and going into debt.

- Option B: Close the account and remove the temptation to spend but let his credit score take a hit.

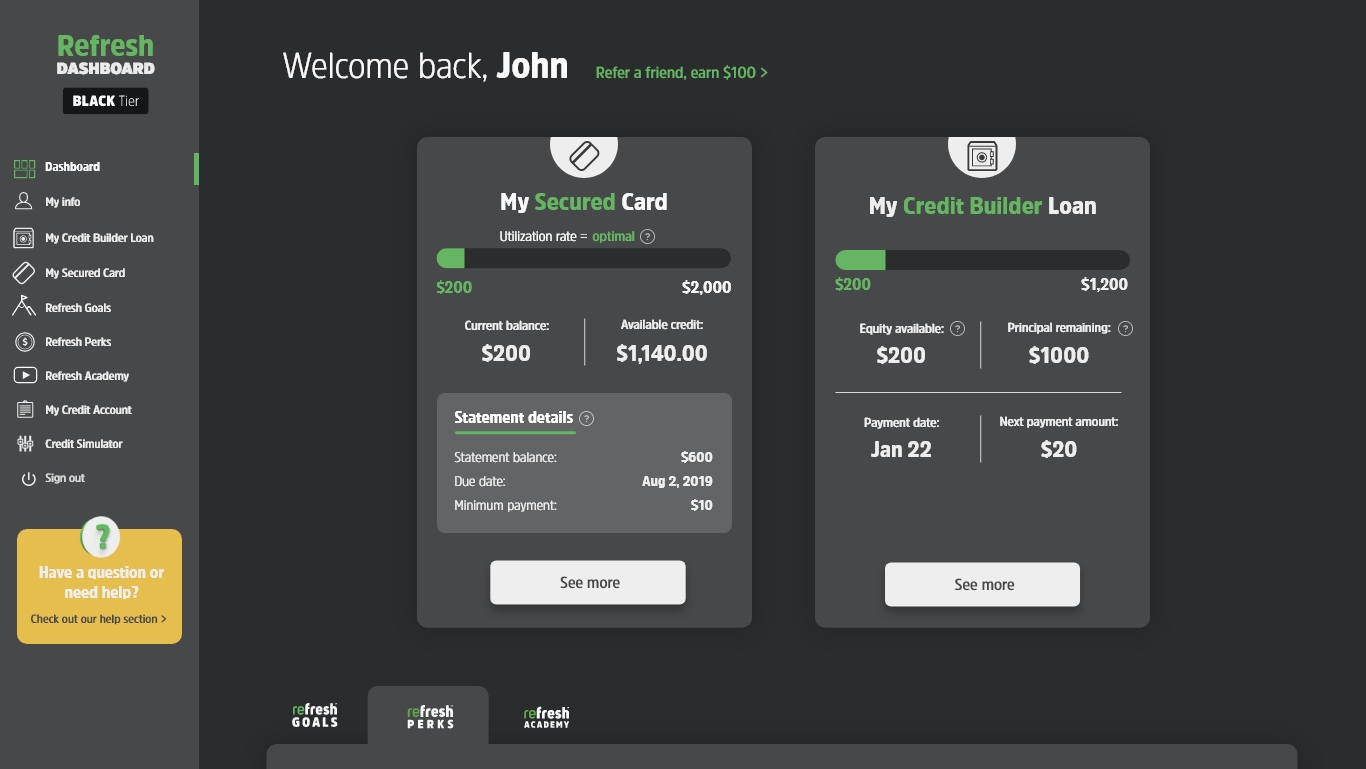

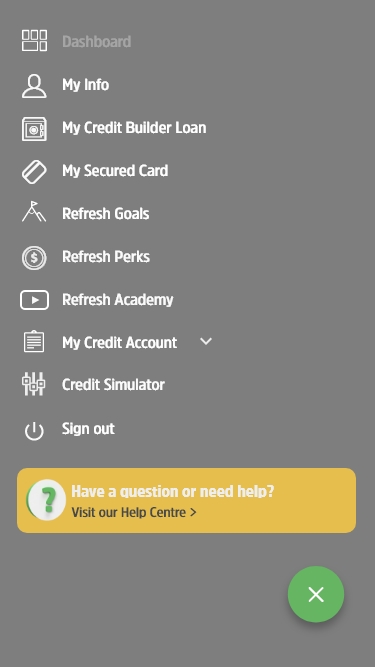

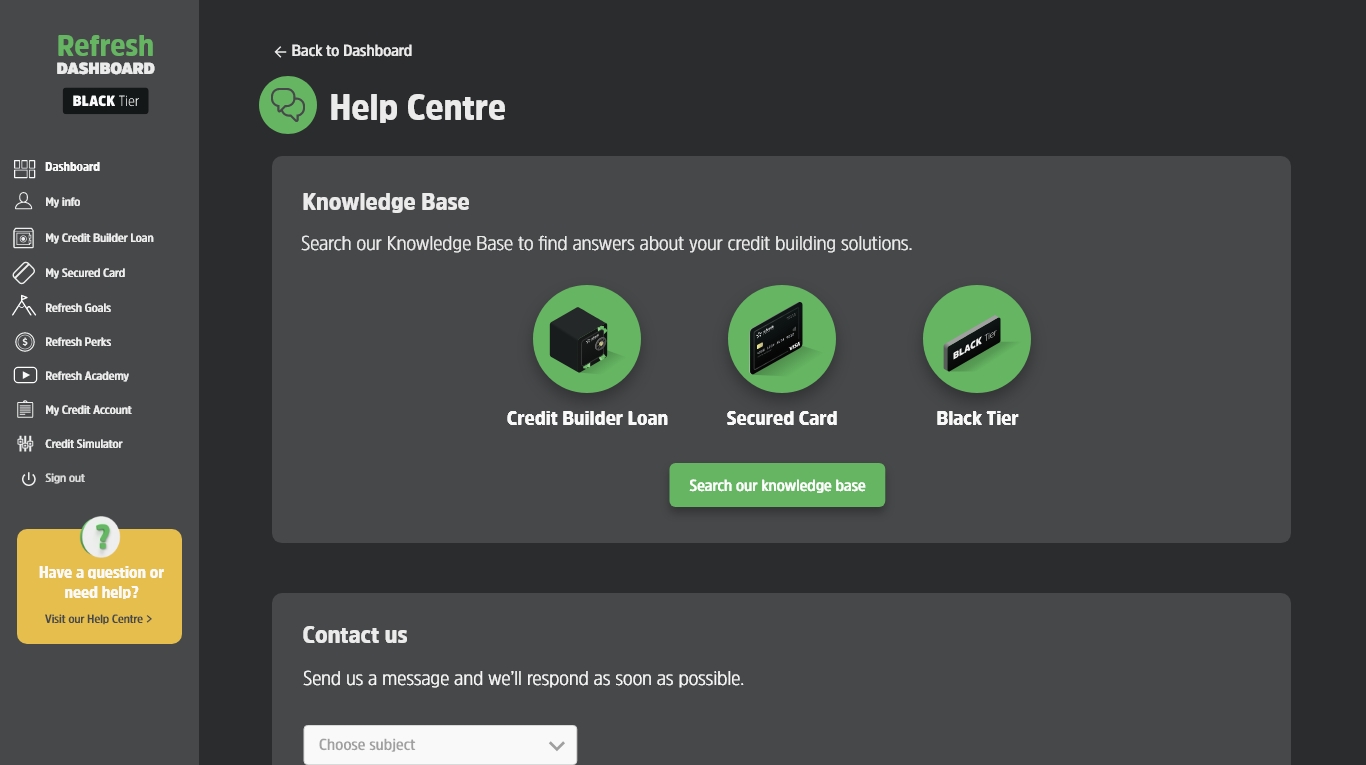

We are excited to officially launch Knowledge Base as part of Refresh Financial’s client dashboard. What is Knowledge Base you ask? Well, you would be forgiven for thinking that Knowledge Base is just a fancy name for FAQs, however, we feel it deserves a more fitting name. These aren’t just your run-of-the-mill Frequently Asked Questions. No, we have gone one step further and answered every possible question we could think of related to Refresh Financial’s products – the Credit Builder Loan and the Secured Card – as well as the Refresh Dashboard and Reporting to Credit Bureaus. We want to answer your questions before you’ve even thought of them with the purpose of providing absolute clarity of our products. For example, many people ask us “How many days does it take to get my secured card deposit back”. The answer is 60-90 days. Fewer people ask us why it takes that many days, but we feel our clients deserves to know more. It takes 60-90 days because first there is a 60-day hold on all deposits before they are processed for refund to ensure all merchant transactions have settled. It can then take up to 30 days for the refund to be processed by Refresh Financial. Being transparent with our clients is one of our top priorities. We aren’t trying to hide anything, so letting you – our valuable clients – know what, where, when, why and how things happen behind the scenes here at Refresh is the ultimate goal of Knowledge Base.

We are excited to officially launch Knowledge Base as part of Refresh Financial’s client dashboard. What is Knowledge Base you ask? Well, you would be forgiven for thinking that Knowledge Base is just a fancy name for FAQs, however, we feel it deserves a more fitting name. These aren’t just your run-of-the-mill Frequently Asked Questions. No, we have gone one step further and answered every possible question we could think of related to Refresh Financial’s products – the Credit Builder Loan and the Secured Card – as well as the Refresh Dashboard and Reporting to Credit Bureaus. We want to answer your questions before you’ve even thought of them with the purpose of providing absolute clarity of our products. For example, many people ask us “How many days does it take to get my secured card deposit back”. The answer is 60-90 days. Fewer people ask us why it takes that many days, but we feel our clients deserves to know more. It takes 60-90 days because first there is a 60-day hold on all deposits before they are processed for refund to ensure all merchant transactions have settled. It can then take up to 30 days for the refund to be processed by Refresh Financial. Being transparent with our clients is one of our top priorities. We aren’t trying to hide anything, so letting you – our valuable clients – know what, where, when, why and how things happen behind the scenes here at Refresh is the ultimate goal of Knowledge Base.How do I access Knowledge Base?

Knowledge Base is available from within the Help Centre of your Refresh Dashboard. You can access the Help Centre in the menu.

Check out the Knowledge Base from your dashboard and let us know if you have any questions that are not answered!

Check out the Knowledge Base from your dashboard and let us know if you have any questions that are not answered!  Join Refresh Academy and Kevin Cochran, Co-Founder of Enriched Academy – an online platform dedicated to delivering inspiring financial education – as we share useful advice and tips each month to help with all aspects of your credit score and finances. Next Webinar: Date: TBD Time: TBD Topic: TBD

Join Refresh Academy and Kevin Cochran, Co-Founder of Enriched Academy – an online platform dedicated to delivering inspiring financial education – as we share useful advice and tips each month to help with all aspects of your credit score and finances. Next Webinar: Date: TBD Time: TBD Topic: TBD What is Refresh Academy?

Refresh Academy comprises convenient, online resources including engaging financial videos that make money concepts simple. Course topics for self-education include:- Money Myths

- Understanding Credit

- How to Save

- Building Wealth

- Careers

- Goal Setting

- Building your Brand

What is credit utilization rate?

Your credit utilization rate is the amount of available credit you have to your name, compared to how much you have used. For maximum credit building, your credit utilization rate should be under 30%.- Your credit utilization rate only applies to your revolving credit. Revolving credit is credit that can change each month. For example, with a credit card or line of credit, you would owe a different amount each month, depending how much of the available credit you used that month.

- Your credit utilization rate is not affected by installment credit like loans and mortgages since it is a fixed amount that is owed on an on-going basis.

- Credit Card – Revolving Credit

- Credit Limit: $5,000

- If balance owing is $1000, minimum monthly payment is $25, credit utilization is 20%

- If balance owing is $2500, minimum monthly payment is $65, credit utilization is 50%

- Your monthly payment – and therefore your credit utilization – changes each month.

As you can see, even though the two credit cards are carrying a balance that makes the credit utilization rate 30% or under, when all three tradelines are combined the credit utilization rate is 45%. In this instance, it would be best to pay down the line of credit as soon as possible.

As you can see, even though the two credit cards are carrying a balance that makes the credit utilization rate 30% or under, when all three tradelines are combined the credit utilization rate is 45%. In this instance, it would be best to pay down the line of credit as soon as possible.Free credit utilization calculator

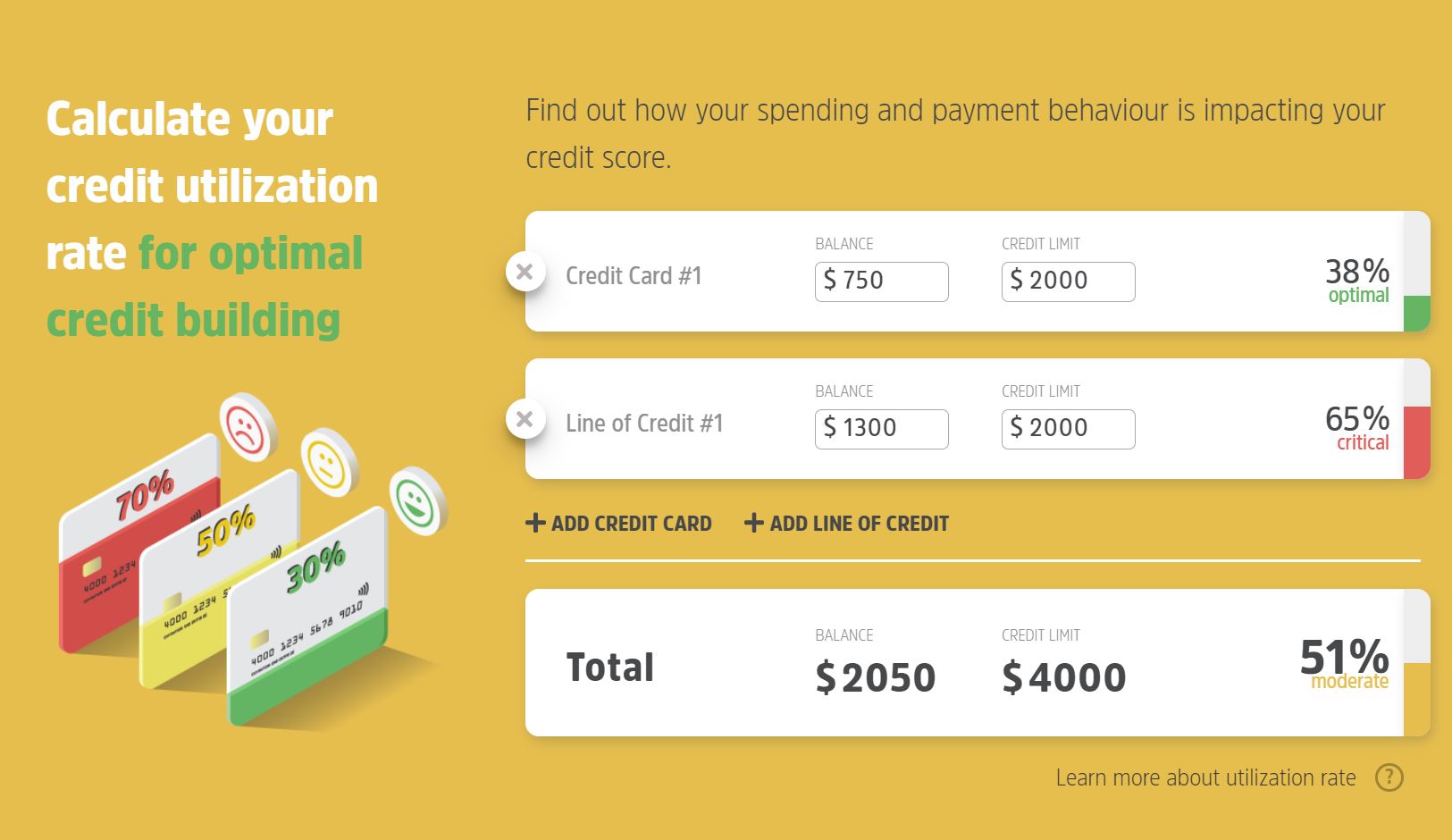

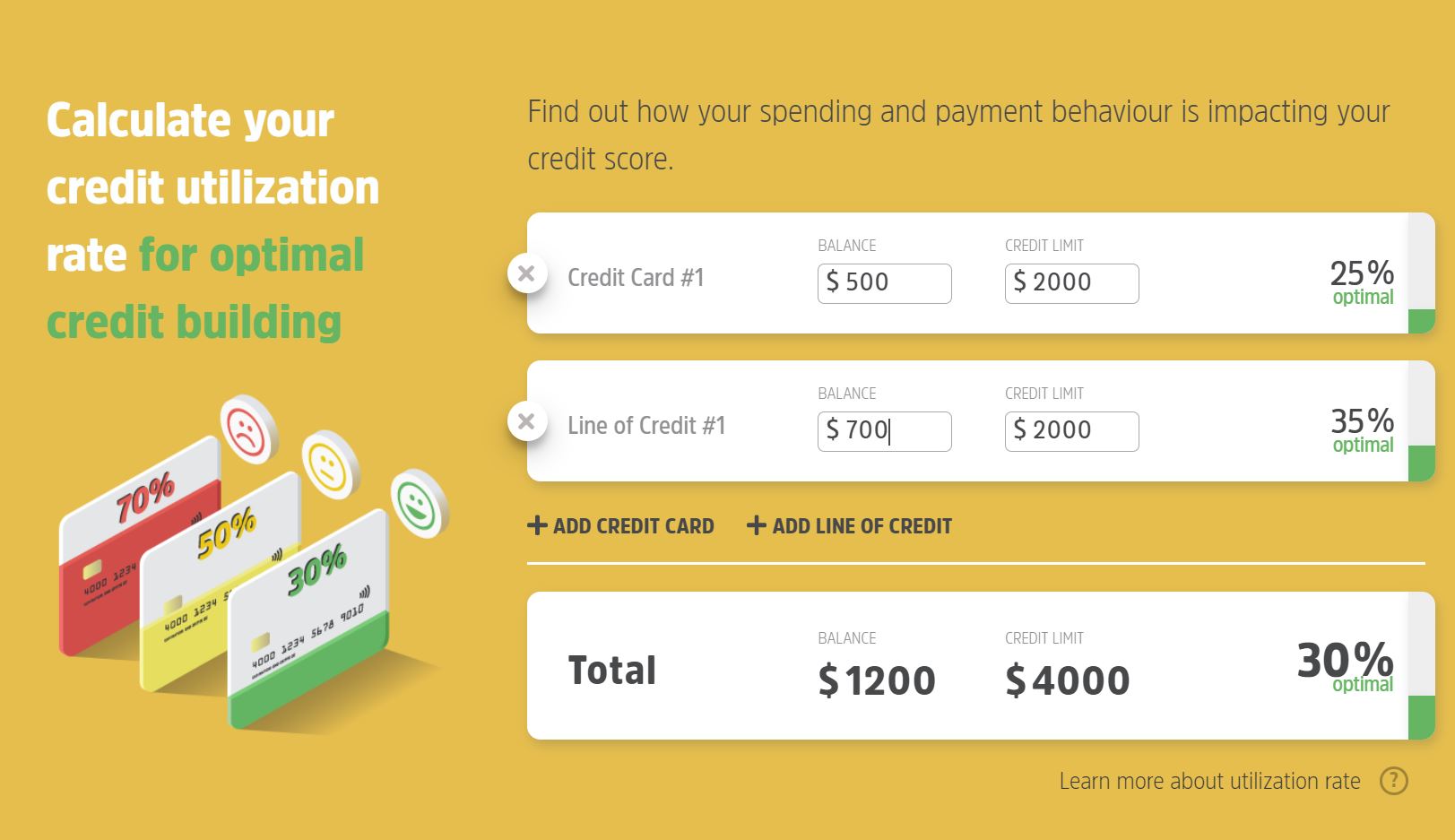

Given the importance of credit utilization rate, we have added a new free feature to our website! With our credit utilization calculator, you can see exactly what your utilization rate is and how much you need to reduce it to get your rate to 30% or less. Find the calculator at https://refreshfinancial.ca/secured-card/ Here you can see the credit utilization rate is 51% when both credit cards are considered: By reducing the balance to $500 and $700, the credit utilization rate drops to 30%.

By reducing the balance to $500 and $700, the credit utilization rate drops to 30%.  This tool is free to use and we encourage you to enter all your sources of revolving credit to see what your current credit utilization rate is! If you do not have a credit card, consider applying for the Refresh Financial secured card. Having a source of revolving credit reporting to the credit bureaus can have a significant impact on your score – not to mention the fact that simply having a mix of both revolving and installment credit impacts 10% of your score!

This tool is free to use and we encourage you to enter all your sources of revolving credit to see what your current credit utilization rate is! If you do not have a credit card, consider applying for the Refresh Financial secured card. Having a source of revolving credit reporting to the credit bureaus can have a significant impact on your score – not to mention the fact that simply having a mix of both revolving and installment credit impacts 10% of your score!

This card is owned and issued by Digital Commerce Bank pursuant to license by Visa International. Use of the card is governed by the agreement under which it is issued. The Visa Brand is a registered trademark of Visa International. All credit and approvals are provided by Refresh Card Solutions Inc. Digital Commerce Bank provides no credit or loans. All funding and lending for this program is provided by Refresh Card Solutions Inc.