What is a secured credit card?

A secured credit card – sometimes referred to as simply a secured card – is just like a regular credit card in that your credit limit, balance and payment history is reported to Equifax and TransUnion and will impact your credit score. With a secured credit card, again, just like a regular credit card, you have a minimum monthly amount due, and as you pay off your card balance, your available credit goes up again. The difference between a secured card and an unsecured credit card is that for the secured credit card, you put down a deposit, usually equal to the limit you want on the card. Check out this post to find out more about the differences between a secured card and an unsecured credit card.What is a prepaid card?

A prepaid card is loaded electronically with a certain amount of funds. You are then free to use the prepaid card like a regular credit card until the funds are gone. No monthly payments, no interest. When you make a purchase, the purchase amount is deducted from your card balance, much like a debit card – you’re not borrowing money from the card issuer as is the case with a secured credit card or regular credit card. Ultimately, because you are not being extended any credit, a prepaid card does not have any impact on your credit score. Why? Because there is no payment history to report – you are not building your reputation as a borrower – you’re just spending your own money.What is the difference between a secured credit card and a prepaid card?

- Credit Building

- Fees

Prepaid card vs secured credit card: which is the better choice for me?

Ultimately, which card works best for you depends entirely on your financial situation. Both a secured credit card and a prepaid card require funds to be put down. The best option for you comes down to whether you want your card to work for you. If you want to build credit as you use the card, the secured credit card is best, however, if you simply want the spending flexibility of a card when a debit card won’t do, and then a prepaid card will be the best. Both cards help to control spending and teach responsible spending habits, as well avoiding debt.What can I do if I have no money to put down?

Unfortunately, if you have poor credit and no money to put down on a credit card, but you’re looking for the spending flexibility of a credit card (i.e being able to buy items on line, and other situations when a debit card doesn’t work) then your credit card options are limited. Nearly all credit cards require either good credit to be able to get an unsecured credit card, or access to funds to put down on a secured card or a prepaid card. Our recommendation is that you work on building your credit score so that you are not limited in your options in the future. Refresh Financial has a Cash Secured Savings Loan does just that and requires no money up front.

If you’re reading this, and you’re a new Canadian immigrant, or you’ve been here a little while as a permanent resident — we want to welcome you!! You’ve likely found out that to build credit as a new immigrant to Canada you need to have a good credit history. If you want to borrow money in Canada, your credit score determines the likelihood of you getting approved for credit products. The good news is that building a credit history as a new immigrant in Canada is easier than trying to improve bad credit history.

If you’re reading this, and you’re a new Canadian immigrant, or you’ve been here a little while as a permanent resident — we want to welcome you!! You’ve likely found out that to build credit as a new immigrant to Canada you need to have a good credit history. If you want to borrow money in Canada, your credit score determines the likelihood of you getting approved for credit products. The good news is that building a credit history as a new immigrant in Canada is easier than trying to improve bad credit history.A Guide for new Canadian immigrants, and permanent residents

1. Understand how a credit score works.

Your credit score is a 3-digit number between 300 and 900 that represents your creditworthiness. The first thing you need to know is how credit scores are calculated. This will help you prepare the right plan so you can build your score quickly. A good credit score is anything over 660. A credit score is derived from the information on your credit report. A higher score means you have demonstrated responsible credit behavior.

2. Factors that make up your credit score:

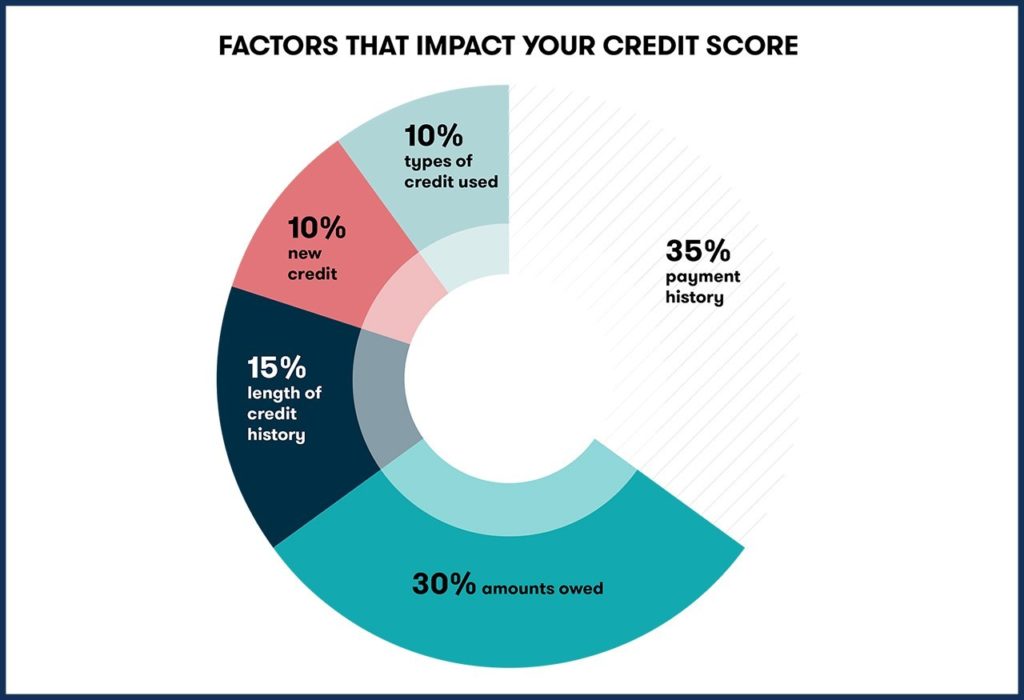

• The history of bill payments determines 35% of your score. The best thing you can do as a new Canadian is to make all your payments on time each month. • The amount of debt accounts for 30% of your score. Stay away from large sums of the debt. It’s better to have more credit available to you than debt. Keep our credit utilization at 30% or less. • The age of your credit history affects 15% of your score. This shows the duration of experience you have with building credit. • New Inquiries determine 10% of your score. Each credit application gets reported. A couple of inquiries won’t affect your score much but if you have lots in a short time it affects your score. • Diversity of credit accounts for 10% of your score. Get a variety of tradelines to show creditors that you understand how credit works. These tradelines can include a loan or a credit card. Make sure you apply for credit only when you need it. It’s important to know what this means for you when you are applying for credit, so check out this great article on a soft credit check versus a hard credit check.

Make sure you apply for credit only when you need it. It’s important to know what this means for you when you are applying for credit, so check out this great article on a soft credit check versus a hard credit check.3. Get a secured card right away, as a new immigrant

Apply for Refresh Cash Secured Card. With a secured card you are guaranteed approval and your credit activities will be reported to both the credit bureaus. There are various financial institutions that offer a secured card. The way the secured card works is that you use your own money as the security deposit on the card and this is the credit amount you have available to use. Using your own funds to build your credit is less risky for creditors while at the same time it helps you manage your money better.

4. Apply for a secured loan program.

It’s important to get a variety of lending products. It shows lenders and creditors that you can borrow money using a variety of credit mix. Having a variety of lending products demonstrates that you are knowledgeable about credit. Refresh Financial offers a secured loan credit building program that uses your own funds to help you build your credit score.5. Apply for an unsecured credit card.

Not everyone who applies for an unsecured card gets approved, especially if you don’t have a credit history in the country you live in. There is a strong chance that the credit card you get approved for will come with a high-interest rate. Make sure you apply for credit only when you need it. Here’s a great article on a soft credit check versus a hard credit check. It’s important that you know what this means for you when you are applying for credit because different types of credit checks affect your credit score.6. Get a cell phone.

There are lots of phone carriers that don’t require credit history, and they will report your paid bills to the credit bureaus. Make sure you are getting a monthly plan that is not pre-paid. You want to get one that you pay off every month as opposed to a one-time pre-paid card. This shows that you are reliable with your monthly recurring bills.7. Apply for a car loan.

You’re going to need a car to get around town. The public transit system won’t get you everywhere you need to on time. When you get a car loan you are building your credit history every time you make payments on your loan. Here are three ways you can apply for a car loan: • You can apply for financing through a dealer. If you qualify you will likely have a higher interest rate on your loan. It’s okay to start by paying more because this gives you the opportunity to build your credit score. • You can also ask your financial institution for a car loan. • Alternatively, you can talk to an independent finance company that specializes in car loans.8. Pay your bills on time.

The best way to build credit as a Canadian immigrant is to make sure you pay your bills on time. This is what creditors and lenders pay the most attention to. It’s the most important way to build trust. Lenders look to see that you are paying your bills on time and in-full. With credit card payments pay more than your minimum payment. As a new Canadian, you likely don’t have debt or items in collections, but it’s good to know that these things affect your credit score.9. Keep on top of your credit score through credit monitoring.

All your efforts to build credit as a Canadian immigrant will pay off if you are diligent about it. Stay on top of your score each month by checking your own credit score. Checking your own credit score is classified as a soft credit check, so it doesn’t negatively impact your score. Credit monitoring will alert you if any fraudulent activities take place on your accounts. If you know about them early enough you can address these issues right away.10. Get your full credit report on a yearly basis.

How often you check your credit report is a bit of a tricky question. As a rule of thumb, you want to check on your credit report at least once a year, to see if there are any errors in your report. To fix any errors you will have to contact either of the two credit bureaus in Canada: Equifax Canada and TransUnion Canada.How long does it take to start using your credit history?

To build credit as a Canadian immigrant will take you a bit of time. Financial institutions will usually start using your credit history after about 18 months. Other factors that different lending or financial institutions consider include your savings, your net worth, income and ability to provide a security deposit or a down payment on a big purchase such as a home. These are all strategies that go a long way towards building a Canadian credit history for new immigrants. If you take the necessary steps we’ve talked about, you’ll start to see a real difference in the rates you pay and you’ll see how easy it is to get credit. Plus, you’ll be a more disciplined spender and more of a saver.Bookmark this page!

When you’ve built your credit history, come back here and do your free credit check with Refresh Financial. Another great resource is the Government of Canda website – they have free workshops from time to time on how to build credit as a Canadian immigrant. To continue to learn about managing your debt and credit score wisely, follow Refresh’s Financial Blog. ******* Refresh financial offers custom credit building solutions to help you build your credit score FAST.

The hard truth is that having either no credit or a bad credit history creates doubt with lenders when it comes to offering you any type of loan. Even if you have a good income, you are viewed as high-risk mainly because of having no credit or poor credit. Understandably, companies have a difficult time working with you if you haven’t borrowed money in the past. Similarly, if they know you have borrowed money and have neglected to pay it back on time, it makes it difficult for lenders to know if you are credit trustworthy. Realistically, it’s easier to build your credit score when you don’t have a history as opposed to trying to improve your existing poor credit history.

The hard truth is that having either no credit or a bad credit history creates doubt with lenders when it comes to offering you any type of loan. Even if you have a good income, you are viewed as high-risk mainly because of having no credit or poor credit. Understandably, companies have a difficult time working with you if you haven’t borrowed money in the past. Similarly, if they know you have borrowed money and have neglected to pay it back on time, it makes it difficult for lenders to know if you are credit trustworthy. Realistically, it’s easier to build your credit score when you don’t have a history as opposed to trying to improve your existing poor credit history.What happens if you do not have a credit history

When you don’t have a credit history, this means that the credit bureaus don’t have anything on your credit report. More specifically, it means that you have not borrowed money in the past seven years, whether in the form of a credit card or loan. There are many people who may not have a need to borrow money, or they haven’t had the opportunity to build their credit; this could be a student or a person new to Canada. Also, there are people who simply do not believe in borrowing money. Even if you have a reliable income but no credit history, you will be seen as a high-risk borrower because you don’t yet have a track record. A lack of credit history can result in:- Issues trying to find a place to live

- Trouble finding work in different sectors

- Higher interest rates if you qualify for a credit product

- Higher deposits on insurance products

How to build a positive credit history

Not having a credit score can be good news because you get to start with a clean slate!Get a secured card

To build a credit history from scratch, you can start by applying for a credit product. The simplest type of lending product is a credit product. If you are not eligible to get a credit card, then apply for a secured card. With a Refresh Secured Card, you are automatically approved. As the name suggests, these cards are backed by a security deposit of your own money. It’s less risky for financial institutions and other creditors to give you a secured card when you’re using your own money to build credit.Sign up for a credit-builder loan

With a secured loan product, you don’t have to put upfront cash as a deposit. This means, you’re still using your own money to build credit and are making installment payments towards a loan.Authorized user status

You can become an authorized user on the credit card of someone else who has a good payment record. They can help you develop your credit score. In this situation, you are not responsible for the payment, and the effect on your credit is limited, but it will give you a jump start.Consider a co-signer

This can be a risky endeavour for the co-signer because they will be entirely responsible for paying off the loan. Also, if they fail to pay off the loan, it could damage your relationship.Pay off your outstanding or late bills

It can’t be said enough times that making all your payments on time each month is crucial to your credit score. On-time and in-full payments not only reduce the money you owe, they also lower your debt-to-credit ratio. Furthermore, if you have any accounts that are in collections, make sure you get those outstanding balances under control quickly.

Bad Credit History

Bad credit history means you have a bad credit score, and this could be the result of a few factors. A bad credit score is between 300 and 629. Potential factors that may have affected your credit score could be missed utility payments or a defaulted loan. If you have had any debt sent to collections, this will also show up on your credit report. There is a lot of value in checking your free credit score and getting your free annual credit report. These two tools can help you understand what type of changes you could make to alter the trajectory of your credit score.Managing Bad Credit

A good credit score is just around the corner! A good score is between 690 and 719. If you want to improve your credit, you need to realize that it takes time and good consistent credit-building behaviour. These are the main elements that make up your credit score.- 35% of your score comes from your payment history. This essentially shows all of your on-time payments, so make sure you pay all of your bills on time and in full.

- 30% of your score comes from the amount you owe. This includes all of your credit products (credit card, car loan, mortgage, other debt). This number is your credit utilization, which shows how much you have available to borrow and how much you owe at any given time.

- 15% of your score is the length of your credit history. This is the duration of time you have spent building your credit. Start building your credit as early as you can.

- 10% of your score is your variety of credit types. This is a combination of personal loans, mortgages, car and credit products. Having a good credit mix will show creditors and lenders that you are knowledgeable about credit and can manage different tradelines.

- 10% is any new credit. This is any new credit that you have recently applied for.

Have you been denied for loans and credit cards over and over again? Or maybe you’ve been told you don’t have good credit and you won’t qualify for low-interest rate products. If you can relate to this, then keep reading to learn what you can do to build your credit score and your financial future.

Have you been denied for loans and credit cards over and over again? Or maybe you’ve been told you don’t have good credit and you won’t qualify for low-interest rate products. If you can relate to this, then keep reading to learn what you can do to build your credit score and your financial future.What is a credit score?

Your credit score is a number between 300 and 900. This score represents everything on your credit report. Your credit score is an important number that can cost or save you money throughout your lifetime. The lower your score, the lower your chances of getting approved for financial products. However, this also means you have a greater opportunity to build your credit score and improve your credit history. You can sign up for Borrowell to find out your credit score for free. Checking your score with Borrowell won’t hurt it.

Why is a credit score so important?

A credit score allows lenders to predict the likelihood for you to pay your bills and loans. This scoring metric essentially identifies your credit trustworthiness. Your credit score is a critical number that allows you to get approved for a credit card, a car loan, a mortgage, and much more. This 3-digit number changes regularly, so it’s essential to stay on top of managing your money by carefully budgeting and only applying for credit you need.Your credit score ranges

Here are the credit score ranges and what they all mean. Also, learn more about what the average credit score is in Canada.- 800-900: You have an excellent score and you can get approved for any product at low rates.

- 720-799: You have very good credit! You will have a lot more credit options to choose from.

- 650-719: You have a good credit score. Lenders will qualify you for lower interest rate products.

- 600-649: You have a fair credit score. You’ll need to work on your repayment history so you can demonstrate that you can be financially responsible.

- 300-599: You’ll need to actively work on building your score.

Factors that affect your credit score

To actively build your credit score, study this list—it’s your bible for improving your score.- Payment history makes up 35% of your total score. This report shows your missed payments and your on-time The best practice is to make all your payments on time and in full, including your credit card debt, loan payments, and any other bills.

- The utilization ratio makes up 30% of your score. Credit usage percentage is the total amount of credit you have to your name versus how much of it you have used. It’s best practice to keep your credit usage below 30%. Anything above this will hurt your score.

- The length of credit makes up 15% of your score. If you’ve been making steady payments (on-time and in-full) towards a car loan or a personal loan for several years, it indicates that you are a responsible borrower, and your score will reflect this. This is exactly why you should start building credit as soon as you can, even if you’re going through bankruptcy or consumer proposal.

- 10% of your score comes from having a variety of credit types. You may think that having many credit cards with higher credit limits to your name is the best way to build credit, but it’s not. It’s better to have a variety of credit types, so, we always recommend getting a credit card and a loan. Credit cards are considered revolving credit, and loans are installment lines of credit with a fixed repayment amount each month.

- Credit inquiries make up 10% of your score. Every time someone does a ‘hard credit check’, your score takes a hit because it looks like you’re desperate to find a source of credit. Hard credit inquiries should be limited, especially if you’re declined after the first one.

What are hard credit checks done on:

- Cash loans

- Credit cards

- Cell phones

- Electricity bills

- Car loans

Tips for rebuilding your credit

- Get the latest copy of your credit report and your credit score. Your credit report will show you why you have bad credit. Knowing why will help you avoid making the same mistakes.

- Review your credit report at least once a year. This will help you stay on top of your score and help you identify any incorrect information on your file.

- If you have missed payments, get on top of them quickly by making at least your minimum payments; it’s better than not paying them at all. If you need help with getting on top of your payments, contact your creditors to see if they can work with you to get things back on track.

- Once you’re on top of correcting your credit score, don’t wait for the negative information to fall off your report — start building your credit immediately. In addition, consider applying for the Refresh Cash Secured Card. This type of credit card will help you spend money responsibly while building your credit score. With a secured card, your money is held as security for the limit on your credit card. Also, all your activities are reported to the credit bureaus to help build your score. Furthermore, if you fail to make payments, your account is closed and paid off using your own money.

- Diversify your credit tradelines by applying for the Refresh Cash Secured Loan. With this credit-building program, you can arrange to make affordable payments, which makes it flexible on your wallet. Each payment you make carries a small interest component. With the interest you pay on each on–time payment, we can report your loan program as an installment loan to the credit bureau. Learn more about the Refresh credit building loan product.

How long does negative information stay on your credit report?

Unfortunately, negative information cannot be removed from your credit report; only incorrect information can be disputed with the credit bureaus. The only way negative items can come off your credit report is by waiting it out or by filing a complaint with The Financial Consumer Canada Agency of Canada.- Accounts in collections can stay on your credit report for up to 7 years.

- Late payments will remain on your report for 7 years.

- Consumer proposals remain for 3 years once the proposal has been completed.

- Bankruptcies stay on your report for 6-7 years, and if you have a second bankruptcy, it will take about 14 years to be removed from your report.

- Auto repossessions can also stay on your report for up to 7 years.

We Canadians focus on high school grades to try to get into a great college or university. And when it’s all done, the next and most important grade we get is our credit score. This is your 3-digit score that signifies whether you have good or bad credit. This score ultimately defines your financial life! That’s why we’re sharing the top 10 things you must absolutely know about your credit. These are things to know about credit because they will drastically change the trajectory of your financial health.

We Canadians focus on high school grades to try to get into a great college or university. And when it’s all done, the next and most important grade we get is our credit score. This is your 3-digit score that signifies whether you have good or bad credit. This score ultimately defines your financial life! That’s why we’re sharing the top 10 things you must absolutely know about your credit. These are things to know about credit because they will drastically change the trajectory of your financial health.1. Get your free credit report

The first thing lenders and creditors do before they decide to give you any money are that they to check your credit history. To get approved for any loan amount, you need to make sure to stay on top of your credit score before applying for any credit. It’s a good idea to get the latest copy of your credit report, which shows your major payment activities on your credit cards and loans. Your report will also show whether you have filed for a consumer proposal or bankruptcy. By federal law, you can request your free credit report once a year.2. Spend less by improving your interest rate

A poor credit score costs you a lot more money because lenders don’t trust you and view you as a credit risk. So, if you end up getting approved for any type of loan, it will come with higher interest rates, costing you a lot of money in interest. On the flip side, if you have a good credit score, you will be approved for a loan with lower interest rates, saving yourself a lot of money. So, don’t wait any longer—let’s improve your credit score.3. Fix errors on your credit report

When you review your credit report, make sure to look at the details and check for any possible errors. Some of these mistakes could include late credit card payments or missed loan payments. You may even find accounts showing on your credit report that aren’t yours. When you find these errors, make sure to report them immediately and have them scrubbed from your credit report.4. Learn the difference between a ’hard credit’ check and ‘soft credit’ check

There are two types of credit checks. When an employer, landlord, select financial institution or insurance agency run a credit inquiry, this is called a soft credit check and it doesn’t hurt your score. However, when you apply for a car loan or personal loan, a hard credit check is performed. This affects your score because it represents the number of times you have asked to borrow money. Learn more about the difference between a hard versus soft credit inquiry.5. Landlords and employers check your credit score

At some point in your life, when you apply for a job or an apartment, your credit is checked. Some employers will do a deeper check before hiring and look into your credit history; it depends on the employer and the type of job you’ll be doing. Employers must ask your permission before doing a credit check. If they decide not to hire you based on your credit, this information must be shared with you. Landlords aren’t required to get your permission before doing a credit check, but they do have to let you know if they are denying your application because of your credit.6. Check your credit score for free

If you don’t know your 3-digit credit score or simply haven’t checked it in a while, then you can check your credit score for free with us at Refresh Financial. You can check your own score at any time without impacting your credit, it’s called a ‘soft credit check’. Also, keep in mind that you get a copy of your free credit report annually. We really recommend that you do.

7. Learn the main factors that affect your credit

- Your payment history affects your credit in a big way. This accounts for 35% of your entire score. Your payment history is a report of all your on-time and missed payments.

- Credit utilization is the second biggest factor, which accounts for 30% of your score. This is how much of your credit limit you have available to use versus how much you have used. Make sure you keep your credit card use to 30% of your total available balance.

- Length of credit history accounts for 15% of your score. Essentially, the longer you have been using credit, the better it is for you. Not having a credit history makes you a higher risk borrower.

- The Credit mix accounts for 10% of your score. It’s best to have a variety of accounts, including revolving debt (like a credit card) and installment loans (like a mortgage, a student loan, or a car loan). Having a credit mix shows that you are a knowledgeable borrower and that you can manage different types of credit.

- New credit accounts for 10% of your score. Watch out for this one. Avoid trying to get a lot of new credit in a short amount of time; spread it out if you need to. You don’t want to look like you’re desperate to borrow money.

8. Learn the things that DON’T affect your credit

Yes, surprisingly, there are things that do not affect your credit score. Some of these include:- The amount of money you make. This has no bearing on your credit score. You can make a lot of money or very little money, and your credit score won’t change regardless. Still, your income can indirectly impact your access to credit and your credit score.

- For instance, a credit card provider will ask you for your income. Then they’ll use it in conjunction with your credit report to decide whether or not to give you a card and what the terms are going to be.

- Your net worth. You could be a movie star with big earnings living in a mansion. This would be fantastic, but it doesn’t affect your credit score. What does affect your score is whether you made the payments on your nice mansion on time and in full.

- Whether you’re on welfare. If you receive income assistance from the government or disability, this has no effect on your credit score.

- The ivy-league you did or did not attend. This information doesn’t get published on your credit report and it doesn’t factor into your credit score.

- Whether you’ve been to jail. Your credit score doesn’t change if you’ve been to jail. Your credit is impacted if you’re sued and owe money, or if your payments are not made while you’re in jail.

- The type of financial institution or financial services you use. It doesn’t matter if you have your finances with a bank or a credit union. As long as you have a credit history, it doesn’t matter where you do your banking.

9. Learn the simple ways to improve your credit score

We talked about the main factors that affect your credit score, and those are very important to keep in mind. Here’s a summary of the top three areas you can focus on when building your credit score:- Pay your bills on time, every time. If you have debt, consistently put money towards your debt to pay it off, even if it means making minimum payments. In case this is not possible, seek a debt consultant or support program to help you.

- If you were approved for a credit card, make sure that you keep your credit usage at 30% of your available limit.

- The other big thing is to build your credit. You can do this by having mixed credit accounts, such as a credit card and a loan. If you currently have poor credit start by getting a secured card and a secured credit-building loan product with Refresh Financial. Here are just a few reasons why a secured card is your best solution.

10. Stay on track and keep fraud at bay

Once you have your credit building products we recommend that you invest in credit monitoring service. This will help you reach your credit goals faster and it will help you detect any identity theft so you can keep your personal information safe. Most credit monitoring services come with extra benefits and perks. Once you sign up with a Refresh credit building product, you can try a 30-day free trial of Refresh Financial’s credit monitoring services and get serious about taking control of your credit score. Now that you are aware of the 10 things you must absolutely know about your credit you can start implementing them one at a time and get set on your road to saving and building wealth, not debt. To continue to learn about managing your debt and credit score wisely, follow Refresh’s Financial Blog. ******* Refresh financial offers custom credit building solutions to help you build your credit score FAST.  Having poor credit doesn’t make you a bad person. It can, however, put a damper on your entire life and affect your ability to get hired, rent or buy a home, and get a low-interest loan. This can feel as though you’re stuck and can’t get ahead. So, if you’re telling yourself “I have bad credit what should I do?”, the best way to combat this is to find out your current score. Once you know your current score, next learn what your score means, and finally start using a credit building program to improve it.

Having poor credit doesn’t make you a bad person. It can, however, put a damper on your entire life and affect your ability to get hired, rent or buy a home, and get a low-interest loan. This can feel as though you’re stuck and can’t get ahead. So, if you’re telling yourself “I have bad credit what should I do?”, the best way to combat this is to find out your current score. Once you know your current score, next learn what your score means, and finally start using a credit building program to improve it.What is a bad score?

Your credit score is a 3-digit number that’s between 300 and 900. Your score is calculated based on many factors. This 3-digit number represents your credit risk or in order words the likelihood of you paying your bills on time. Your score is calculated using the information from your credit report. Your report looks at your payment activities, the amount of debt you have, the length of your credit history, and a few other things (see infographic below for a full picture). The higher your score is, the greater your chances of getting the financial products you want at low-interest rates. Here are the score ranges:

The higher your score is, the greater your chances of getting the financial products you want at low-interest rates. Here are the score ranges:- 300-579: Poor

- 580-669: Fair

- 670-739: Good

- 740-799: Good

- 740-799: Very good

- 800-850: Excellent

I want to get a free score!

I want to get a free score!Things you can’t access with a bad credit score:

- Any kind of credit (cash and car loan)

- Make big purchases (home and car)

- A low-interest rate (this is impossible to achieve. All your financial products will come with higher interest rates, therefore, costing you more money). See the infographic below to see how much interest you might be able to save with good credit

- Low insurance premiums (your annual fees may be through the roof when it comes to insurance products)

Why do I have a bad score?

There are many things that can contribute to your bad score. Some of these include a filed consumer proposal, bankruptcy, negative payment history, a large amount of debt to credit ratio, or errors on your report. If your score is low because of missed payments, then it will take more time to improve your score. However, if it’s low because of errors on your report, then make sure to consult with the reporting agencies within 30 days and get these issues corrected immediately.What’s a good score?

A good score is anything above 670. The good news is that there are plenty of ways to increase your score. Firstly, start by checking your score. When you check your own score, it’s called a soft credit check, and it doesn’t hurt your score. Secondly, if you don’t have a good score, you can start building it with a Refresh Secured Card or a Cash Secured Loan program. Lastly, on a yearly basis, get a copy of your report from the credit bureaus—this is what lenders consider when they review your applications.How do I get a good score?

Once you know your starting score, here are a few things you can do to improve it to the Good, Very Good or Excellent categories:- On-time payments—the best way to improve your score is to pay your bills before their due date and pay off debt as soon as you can. If you decide to pay off your debt gradually, make sure you’re making a dent in it by paying the principal. If you have various types of debt, check out this article on how to prioritize your debt payoffs. Pay close attention particularly to medical and utility bills, and don’t let them go to collections. Your payment history makes a huge difference in your score, it accounts for 35% of your total score.

- Credit Utilization—any credit usage over 30% will harm your score. This doesn’t mean you have to spend less—it means you should pay off your card balances multiple times per month so you’re on top of it. This makes up 30% of your overall score.

- Credit Age—if the age of your credit is bringing down your score, hold off on closing any of your credit cards. You may think this will help close any debt, but quite the contrary. This accounts for 15% of your score.

- New Application—applying for too many accounts in a short time period can hurt your score. Because every time you apply for a regular credit card there is a hard credit check. Stop applying for new credit until your score has increased. This accounts for 10% of your score.

- Types of Credit Mix—it’s a good idea to diversify your accounts. Start with a revolving product, which is a credit card, and then add a loan, which is an installment tradeline.

How long does it take to clear up a poor credit history?

Even if you raise your score, your report may show some negative items that simply take longer to come off. Take a look below:- Bankruptcy—10 years from the filing date

- Consumer Proposal—3 years from the filing date

- Collection accounts—180 days plus 7 years after the first payment was missed on the original account

- Credit inquiry—2 years after the inquiry was authorized

- Debt settlement—7 years after the final date of discharge

- Defaulted federal student loan—7 years from the first date of delinquency, or until you bring the loan current

- Foreclosure—7 years from the date when the account first became delinquent

- Late payments—payments 30+ days late are reported and can remain for 7 years

- Missed child support payment—7 years from the original delinquency date

- Unpaid tax lien—can remain indefinitely, and may be removed after 15 years

- Unpaid court judgment—may remain indefinitely

Have you ever applied for a credit card and were told that your credit will be checked to see if you are approved, or that there might be a ‘hard’ inquiry? You might be asking yourself, what’s a hard inquiry? Are their soft inquiries? What’s the difference? In this article, we will take a closer look at what credit inquiries are all about, we’ll explore the different types of credit checks and discuss how they impact your score.

Have you ever applied for a credit card and were told that your credit will be checked to see if you are approved, or that there might be a ‘hard’ inquiry? You might be asking yourself, what’s a hard inquiry? Are their soft inquiries? What’s the difference? In this article, we will take a closer look at what credit inquiries are all about, we’ll explore the different types of credit checks and discuss how they impact your score.What is a credit inquiry?

A credit inquiry is when an organization or individual requests to see information stored in your file. This is a ‘credit check’. This check is done to learn more about your payment habits.What is a credit score?

Your credit score is a number anywhere between 300 and 900. This number represents your “credit trustworthiness” – this is the credit history that’s on your credit report. Your credit score is created by a computer that reviews various criteria on your credit report and converts all that information into one simple score. Your score is typically based on these five main factors:- Payment history – 35% of your score

- Amount of money you owe versus what you have available, better known as your credit utilization – 35% of your score

- Length of your credit history – 10% of your score

- Types of financial products and tradelines – 10% of your score

- Account inquiries – 10% of your score

What is a “soft” credit check?

There are two types of credit checks: soft credit checks and hard credit checks. A ‘soft’ check takes place when a potential landlord, employer, insurance company, pre-approved credit card companies, or if you request to see your credit score for informational reasons. These soft checks are purely for informational reasons and not for the purposes of assessing your risk. Soft checks can occur without your permission and they do not negatively affect your score — they simply help with your pre-approval or qualification. Actually a good habit to get into is to check your own score (which is a soft credit check) and monitor your history. You’ll be able to catch any errors in your report. This will help you remain in good standing.

What is a “hard” credit check?

Lenders will want to assess your level of risk when looking to lend you money. Higher risk means you may pay more in interest, or it could mean that you may be declined outright. Lower risk means access to higher borrowing amounts and better interest rates. The lender will determine your level of risk based on your score. When you submit a credit card application or a lender checks your report through the two major bureaus, this is a ‘hard’ check. These types of checks require your permission before they are carried out, and they can reduce your score. If you are trying to build your score, then stay away from doing too many hard checks.Do multiple inquiries impact your score?

In Canada, when you shop around for mortgages, student loans, and auto loans, the same inquiry process doesn’t apply as it would when you apply for a credit card. With a regular credit card, every credit card application counts towards your score and this is a hard check. With loans (mortgage, auto, and student loans), as long as you’re shopping around and you don’t take the loan offer within 30 days, the inquiries won’t affect your score. Also, if your report shows inquiries older than 30 days, this counts as only one inquiry. Learn more about how credit inquiries affect your score.Reduce your hard inquiries

Too many inquiries can make you appear desperate because a hard check indicates that you are actively looking to borrow money. Hard checks can remain on your report for up to six years. If you want to build your credit, then reduce your hard inquiries. Credit bureaus offer both financial institutions and a few creditors the opportunity to do a soft inquiry on behalf of their clients. This way you can see what product offers are available to you without formally applying for them.Check your score before you apply

Something to avoid is the ‘apply until you get approved’ strategy. You can check your Equifax credit score for free by signing up for Borrowell. Once you’ve signed up, you can quickly compare loans and credit cards before you apply, which can help you limit the number of hard credit checks made on your report. Checking your credit score with Borrowell is a soft credit check, so it doesn’t impact your score. When you know your score in advance it gives you an idea of whether you are going to be approved for the financial products you’re after. And, whether it’s worth the hard check once you apply.Get approved without a hard credit check

Do you have a poor credit history, and are struggling to get approved for financial products? Start by building your score with a secured card. Secured cards are different than prepaid cards and other credit cards. With a secured card, you use your own money to put a deposit on the card. The amount of the deposit is equal to the limit on the card. Not all secured cards are the same. Some of the companies that offer secured cards will do a hard check. However, with the Refresh Cash Secured Card, you’re automatically approved without doing a hard credit check. The Refresh Cash Secured Card comes with a low-interest rate and low fees. And, all your payment activities will be reported to both Canadian bureaus to help you build your score. Learn more about Refresh’s Cash Secured Card it will help you spend while building your score.

Learn more about Refresh’s Cash Secured Card it will help you spend while building your score.Reverse the damage from numerous credit checks

You can’t reverse the damage, the only way to allow your score to recover is with time. Wait as long as you can before incurring more inquiries on your credit. This means you may have to wait a few months before applying for additional financial products. In the meantime, continue to work on paying your bills on time, and keep your credit utilization ratio within 30%. To continue to learn about managing your debt and credit score wisely, follow Refresh’s Financial Blog. ******* Refresh financial offers custom credit building solutions to help you build your credit score FAST.  With household debt on the rise in Canada, it’s time to take a look at some of the causes. Why do Canadians find themselves buried in debt? How do you manage debt and build up your credit score? Here are some proven ways to take control of your debt and build a positive financial future.

With household debt on the rise in Canada, it’s time to take a look at some of the causes. Why do Canadians find themselves buried in debt? How do you manage debt and build up your credit score? Here are some proven ways to take control of your debt and build a positive financial future.1. Use your credit card properly

This is probably the most common cause of consumer debt. Instead of using a credit card as an alternative method of accessing your money, you may be using it to expand your spending capacity. This can get you in big trouble! The easiest thing to manage is your spending. If you’re using your credit card for day to day spending, ensure that you make your monthly payments on time to avoid high-interest rates. Also, stay well below your credit limit — keep your credit utilization below 30%. The credit utilization ratio is the amount of credit you have used to the amount you have available. Keeping it on the lower side will help you sustain a get credit score. Learn more about how you can be strategic with your credit card usage.2. Pay more than your minimum monthly payment

If you carry the average credit card balance of $15,000 with a typical 15% APR and make the minimum monthly payment of approximately $600, it will take you close to 13.5 years to pay off the money you owe! Debt relief won’t be anywhere in sight. And that’s only if you don’t keep spending extra money and adding to the balance, which can be a challenge all on its own. Whether your money on your credit card, personal or student loans, pay them off by making more than the minimum monthly payment. Doing this will help you save on interest throughout the life of your card or loan, and it will also speed up the payoff process. To avoid any potential headaches, make sure your loan doesn’t charge any prepayment penalties before you get started.3. Make payments on time

Missed payments mean late fees and could even lead to your account being sent to collections, where interest will pile up on you. Also, missed and late payments will end up on your credit report with the credit bureaus. Before you know it, you’ll be in more debt than you can handle. Your negative payment history will damage your credit score, and a poor credit history means you’re considered a credit risk to lenders. If you’re not sure where you currently stand with your credit score, Refresh can check it for you for free. It goes without saying that paying your bills on time is a big deal! One easy way to make sure you pay your bills on time is to set a reminder on your phone. Another is to set up automatic payments on specific days — that way you can relax knowing you’ll never miss a payment again. Most financial institutions have payment reminder apps and tools that you can use to avoid late or missed payments. 4. Have an emergency savings fund

Whether you’ve lost your job or your car needs repairs, an emergency can send your finances into a tailspin. This is why most of us rely on our credit cards for emergencies. Save for an emergency fund, instead of going into debt. Start small. This can be as little as putting aside $20 a month. Build up your savings so you have about three to six months’ worth of your financial obligations. That way if you lose your job or your car breaks down, you’re still going to be able to make all your payments. It’s one of the best ways to manage debt and build credit.5. Give up your expensive habits

If you’re in debt and consistently coming up short each month, evaluating your habits is a great place to start. No matter what, it makes sense to look at all the ways you’re spending money daily. If you don’t track your spending, you won’t know where it all goes. If you do track it, you can evaluate whether those purchases are worth it — and come up with ways to minimize or get rid of them.6. Ask for a lower interest rate on your credit card

If your credit card interest rates are so high it feels almost impossible to make headway on your balances, it’s worth calling your card issuer to negotiate. Asking to have your interest rates lowered is quite commonplace. And if you have a good history of paying your bills on time, there may be a good chance of getting a lower interest rate. Remember, that the worst anyone can say is no. The less you pay for your fixed expenses, the more money you can put towards your debts. If you haven’t used a budgeting app before, give it a try. It will help you budget your household expenses, prevent overspending, get you out of debt, and encourage you to grow your savings. Take a look at PocketGuard and start organizing your bills and save money. Avoid causing yourself more stress and start creating a bright financial future by being proactive and following these guidelines. To continue to learn about managing your debt and credit score wisely, follow Refresh’s Financial Blog. ******* Refresh financial offers custom credit building solutions to help you build your credit score FAST.  Building a good credit history as a student is one of the most important things you can do for yourself. When you want to buy a car, get a personal loan and purchase your first home, lenders will look at your credit report. Start with finding the best student credit card to build credit. I know, it sounds like it’s all in the distant future, but it takes time to build credit. And, the best time to build your credit is when you’re still a student. For instance, when you’re ready to buy your first car, auto lenders will want to see your credit history and your credit score. Without a credit footprint, it is difficult to get the things you want. So, here are a few pointers to guide you on the best way to safely build your credit score and ensure that your education is meaningful.

Building a good credit history as a student is one of the most important things you can do for yourself. When you want to buy a car, get a personal loan and purchase your first home, lenders will look at your credit report. Start with finding the best student credit card to build credit. I know, it sounds like it’s all in the distant future, but it takes time to build credit. And, the best time to build your credit is when you’re still a student. For instance, when you’re ready to buy your first car, auto lenders will want to see your credit history and your credit score. Without a credit footprint, it is difficult to get the things you want. So, here are a few pointers to guide you on the best way to safely build your credit score and ensure that your education is meaningful. 8 tips on how college students can build credit

1. Choose the best student credit card to build credit

Different credit cards have their own unique perks and reward programs, so it’s important to find a student credit card that works for you. When you apply for a card, the best option is to find a card that will help you spend money responsibly. That way you’re not always carrying a balance, which means you’re building a positive credit history. There are so many card options and many card issuers, so how do you decide on the best student credit card? There are cards that offer Scene points for free movies, cashback on all your purchases and much more. Choosing the right card as a student involves making sure you’re spending money responsibly and building your score. Try not to get distracted with all the other perks. There may be hidden or high fees associated with these offers. Instead, check out the Refresh Cash Secured Card option. This option offers low-interest rates, a low annual fee, and reports your payment activities to both Canadian credit bureaus to help you build credit.2. Keep your credit utilization within range

A good credit utilization ratio is less than 30 percent. This means using less than 30 percent of your credit limit. So, on a card with a $1,000 limit, when you keep your balance below $300 you’re within the 30% credit utilization ratio. If you regularly go above this, it may negatively impact your score on your credit report. Learn more about credit utilization and how it impacts your score.3. Create a living budget

Create a budget and stick to it. Make sure to make your card payments on time to avoid high-interest rates. Money may be a bit tight while you’re studying, remember to stay focused. Sacrifice now to ensure a healthy financial future. Trust us, you’ll thank yourself later.4. Look for financial opportunities at school

Are you on a scholarship program? Have you researched and applied to see if you’re eligible? Grant money is a financial game-changer — it can help fund your schooling. Scholarships are available at most schools, and it’s worth the effort to see if you qualify.5. Search for a job

Did you know that some schools offer on-campus earning opportunities? If that’s not an option, usually the surrounding off-campus areas will offer part-time work for students. Finding a part-time job while going to college will help you have disposable income so you can spend and save money while building your score.6. One credit card is plenty

Every time you apply for a credit card, your score will take a slight hit because of the hard credit inquiry to the two Canadian credit bureaus – this inquiry shows on your credit report and can impact your credit report. Do your research before applying for any financial products and stick to just one card. Because we are recommending that you stick to one card make sure it’s the best student card to build credit. There are lots of card options available with cashback offers, but they may have hidden fees and high-interest rates attached to them, so watch out! It’s best to look for a credit card issuer such as Refresh Financial who doesn’t do a hard check and also offers a credit building program.7. Use your student loan for essentials

You need groceries, textbooks and a place to live. Remember, your loan is intended to cover what you need, and not what you want. Use your loan responsibly and pay it back on time. Focus on improving your score in college, so when you graduate, you have a lot of low-cost borrowing options.8. Find ways to pay down your debt

Generally speaking, six months after your final college semester is when it’s time to start paying back your student loan and any other debt. Check out this great article on how to pay down your debts. It’s filled with helpful student debt advice. ******* Refresh financial offers custom credit building solutions to help you build your credit score FAST.  Your credit rating in Canada is a number between 300 and 900, which represents everything on your credit report. Your score is created by a computer program that reviews what is on your credit report and converts all that information into a score. To see where you stand, you can compare your credit score against the average credit rating in Canada. The average credit rating in Canada is around 650 according to both credit bureaus, and this varies from province to province. Once you have increased your credit score to 650 or higher, you’ll be able to qualify for more financial products. A credit score below 650 is going to make it hard to qualify for new credit, also anything you are approved for will likely come with very high-interest rates. Do you know your current credit score? If not, check your free instant credit score with Refresh Financial.

Your credit rating in Canada is a number between 300 and 900, which represents everything on your credit report. Your score is created by a computer program that reviews what is on your credit report and converts all that information into a score. To see where you stand, you can compare your credit score against the average credit rating in Canada. The average credit rating in Canada is around 650 according to both credit bureaus, and this varies from province to province. Once you have increased your credit score to 650 or higher, you’ll be able to qualify for more financial products. A credit score below 650 is going to make it hard to qualify for new credit, also anything you are approved for will likely come with very high-interest rates. Do you know your current credit score? If not, check your free instant credit score with Refresh Financial. What determines your credit rating in Canada?

Here’s a quick summary of how credit works in Canada: 1. Payment history makes up 35% of your score. Paying your bills on time and in full will boost your credit rating. Anything other than this will negatively affect your score. 2. The credit utilization ratio makes up 30% of your score. Credit usage percentage is the total amount of credit you have to your name versus how much of it you have used. For the best impact on your credit rating, bring your credit usage below 30-35%. 3. The length of credit makes up 15% of your score. If you’ve been making steady payments (on-time and in-full) towards a loan for several years, it indicates that you are a responsible borrower, and your score will reflect that. This is a good reason why you should start building credit as soon as possible, even if you’re a student or going through a bankruptcy/consumer proposal. 4. Various different types of credit products make up 10% of your score. Credit cards are revolving credit. You want both a revolving trade line as well as an installment line, such as a loan with a fixed repayment amount each month. Having a variety of credit products will have the biggest impact on your score. 5. Credit inquiries make up 10% of your score. Every time someone does a ‘hard check’ on your credit, your score takes a hit as it can look like you’re desperate to find a source of credit. Limit your hard inquiries, particularly if you have been declined. Hard credit inquiries include:- Cash loans

- Credit cards

- Cell phones

- Electricity bills

- Car loans

What is a “good” credit rating in Canada?

To have a good credit rating in Canada you want to aim for a credit score above 700. Even though “good” technically starts at 660, getting your credit score above 700 is going to open up many new options for you. If you have a good credit rating in Canada, you have access to far better interest rates across all financial products – saving you thousands in the long run. Even more, you get a better chance of getting approved for credit products that you really want.Understanding credit score ranges in Canada

The range of credit scores you can have in Canada is between 300 and 900, the higher the better. Here’s a quick breakdown of what each credit score range means:Excellent credit (760-900)

If your credit score falls within the excellent range, the world is pretty much your oyster. You are guaranteed approval for any financing you apply for when your income supports the payments. You’re also going to be offered the best interest rates and be able to save cash on your borrowed money.Good credit (725-759)

If your credit score is good, you’re still going to get decent interest rates, but it’s worth it to spend a short period of time working your way up to excellent credit – just to be able to unlock even better interest rates. The few months of being patient and disciplined could save you thousands of dollars.Average credit (660-724)

Similar to a good score, you’re probably going to get approved for credit you apply for and you might get some okay interest rates, but it wouldn’t take you that long or very much pain to get up there to a better score. Take the time to build your score from here, then apply for credit.Poor credit (560-659)

You likely won’t be approved for much, outside of secured credit products with scores in this range. Interest rates you’re offered will be high.Very Poor credit (300-559)

Similar to the poor range, your score is going to deny you any product or limit you to secured credit products with very high-interest rates.4 ways to build your credit rating in Canada

If you’re on the lower end of the credit score spectrum, the good news is that your situation is reversible. Even those who have been through a bankruptcy or consumer proposal can recover and can do it quicker than you might realize. Take a look at the Refresh Credit Builder Program for options.1. Check and understand credit reports and scores

There are two credit bureaus in Canada – Equifax and TransUnion. All your financial activities are listed in these reports. For example, if you open a bank account or apply for a credit card, this is listed in your credit report. Lenders go to the two credit bureaus and check your report before deciding to give you credit.2. Keep a low credit card balance

The rule of thumb is to keep your credit to less than 30% of your available limit. Making consistent payments on your credit card month after month – ensuring not to max out your card – will help boost your credit rating.3. Get a secured card

One of the easiest ways to build or rebuild your credit is by opening a secured card account. A secured card is the perfect solution if you are working on building your credit or you are having a hard time getting a credit card. With a secured card, you are required to put a security deposit on your card, and this is the maximum credit that’s available for you to use. A secured card helps you spend money responsibly while building your credit score.4. Monitor your credit score

Your credit score gives you a picture of the overall health of your credit. You can get your free credit score from the two credit bureaus in Canada. Another quick way to get your credit score checked is through Refresh’s credit score checker. You now have all the information you need about credit scores in Canada. You’re even more equipped and confident to start improving your credit and unlocking access to financial products at better interest rates. ******* Refresh financial offers custom credit building solutions to help you build your credit score FAST.

This card is owned and issued by Digital Commerce Bank pursuant to license by Visa International. Use of the card is governed by the agreement under which it is issued. The Visa Brand is a registered trademark of Visa International. All credit and approvals are provided by Refresh Card Solutions Inc. Digital Commerce Bank provides no credit or loans. All funding and lending for this program is provided by Refresh Card Solutions Inc.