Official blog of Refresh Financial

Why Is My Credit Score Not Increasing – and Could it Be Costing Me Money?

Have you researched how to increase your credit score and still find yourself asking, why is my credit score not improving? Maybe you’ve been checking your score regularly and not seen any growth over the course of months or even years?

It doesn’t make sense because you’ve sacrificed and become more disciplined with your money. Maybe you’re being paid more and have a better job. Every time you check your score, you expect to see it’s gone up, but you’re disappointed to see no change. What’s going on? Why is your credit score not increasing?

Well, there are many possible reasons why your credit score may not be increasing. Here are some of the most common reasons:

1. You may have missed some details

It’s very, very important when trying to improve your credit, to obtain your credit report from both TransUnion and Equifax. Every Canadian is entitled to a free credit report from each of these credit bureaus, every year, so grab yours. While it doesn’t contain your credit score itself, it does contain your credit history. If you've asked, 'why is my credit score not improving?', you may have missed something. Go through it with a fine-toothed comb. Clear up any issues that are there and make sure that everything listed on your report is actually you.

You’d be surprised to know how often identity theft occurs and goes unnoticed. Maybe someone signed up for a cable account in your name and defaulted on their bills. Perhaps someone used your credit card number to spend enough to max out your card. For these reasons, being clear on the details of your credit report, along with your credit card statements and bank account statements is the most important first step in how to increase your credit score. Don’t just check these things once, either. Do it as often as you possibly can.

2. Rethink your credit building strategy

Keep attempting to find out how to build your credit in more ways. There are ways to build your credit score fairly quickly, such as secured cards, secured lines of credit, or secured savings programs, like the one Refresh Financial offers. When considering how to increase credit scores, give serious thought to including one or two of these options in your strategy. If you keep your bills paid on time, and take on one of these credit building products, your score should start climbing within a few months.

3. You’re still utilizing too much credit

Your credit usage is a key factor in determining your credit score. If you have $10,000 in credit, and you’ve used $9000 of it, your credit usage is at 90%. This is way too high, and needs to be brought down to at least below 50%. Ideally, bringing your credit usage down below 30% is going to see an almost instant positive effect on your credit score. Often, the answer to 'why is my credit score not improving?' is high utilization.

4. Something from your credit history is at play

When it comes to bankruptcy or a consumer proposal, there is nothing you can really do to avoid the negative impact it has on our credit score. For a bankruptcy, you are going to have to wait six years before it’s removed from your credit report. For a consumer proposal, it’s only three years. You may also have something you’ve defaulted on in your credit history - perhaps you’ve had a credit account sent to collections because you stopped paying. Maybe you’ve got a utility bill in collections. Whatever the case, items such as these in your credit history are going to affect you for a very long time and make credit building more difficult. It is best to settle them up and get them off your credit report.

5. There are errors on your credit report

Your creditors can and do make mistakes. Credit bureaus also make mistakes. Going back to point one, make sure that everything on your credit report is true. If it’s not, take it up with the creditor it came from or dispute it with the credit bureau. Both Equifax and TransUnion have dispute processes that are simple to follow on their websites. Correcting these sorts of errors can make credit building a lot easier.

6. You’re still paying the minimum payments

While paying your bills on time is great, just scraping by with the bare minimum isn’t going to do much for your score. Instead, pay down your debts. Make sure the amount of debt you have is steadily decreasing as much as you can possibly handle.

Credit building is like an engine with many moving parts, and it doesn’t really work if all the parts aren’t there. It all has to come together to get that credit score headed upward. Make sure your credit building strategy is well-rounded, and includes all the best practices, not just some, and you will see a better credit score in just a few months.

If your score isn't increasing, it could actually be costing you money.

How? Your credit score directly affects the interest rates you’re eligible for. Yet another perk of having great credit, is that when you apply for a credit card, you’ll be offered a much better interest rate than someone with poor credit. This can have a huge impact on your financial stability, lowering your overall cost of borrowing significantly.

High-Interest vs Low-Interest

Let’s say you have a credit card with a 19% interest rate and you’ve got a $3000 balance on it. Your minimum payment is 3% or $90. If you pay the minimum payment each month, you’re paying $47.50 in interest every month, and $42.50 goes towards paying down your principal.

Let’s switch that rate for a lower interest rate, let’s say 8.9%. Your monthly payment of $90 is broken down like this: $22.25 of it is interest, while $67.75 goes towards paying down the principal.

With the higher rate, you’re looking at paying your principal down almost six years. With the lower rate, you’re looking at three and a half years and a savings of more than the principal itself. You would save over $3000 with the lower rate in this scenario.

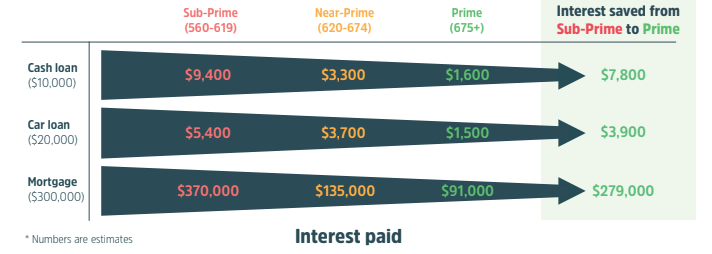

Saving You Money

That’s not the only way having a great credit score can save you money. Here’s a helpful diagram that simplifies the many ways you can save yourself loads of money if you have a good credit rating.

Still wondering how to increase credit score? We can help improve your credit score and get you right back on track.

This card is owned and issued by Digital Commerce Bank pursuant to license by Visa International. Use of the card is governed by the agreement under which it is issued. The Visa Brand is a registered trademark of Visa International. All credit and approvals are provided by Refresh Card Solutions Inc. Digital Commerce Bank provides no credit or loans. All funding and lending for this program is provided by Refresh Card Solutions Inc.

Leave a Reply